Johannes Wessels

@johannesEOSA1

The centrepiece of the Ramaphosa government’s recovery and economic resuscitation scheme – the loan guarantee fund – is as helpful as giving a desperately hungry infant a dummy, pretending it is food. Not even 5% of formal registered businesses have applied for funding and by end November about 1.8% of these firms have obtained assistance from the scheme.

It is far more affordable to cut Company Income Tax and to raise the VAT threshold to get the economy growing again, than to continue with the current package of the Economic

Why the low interest in the Loan guarantee fund?

On the one hand the enterprise world was pre-lockdown already coping with difficult conditions due to an unfriendly enterprise environment with a president that is on record that he disagreed “with the view that the most effective and efficient way to provide services to our people is through the private sector.” Many business owners, especially in the case of SMEs, are reluctant to take on more debt in such circumstances, especially when running also the risk that their properties may be confiscated (expropriation without compensation).

On the other hand, the government, being out of pocket and not keen on disbursing billions that it would lose if the beneficiaries cannot service the loans, had asked the banks to apply their own existing loan assessment criteria when evaluating the applications. Were it a Khula or a SEFA process, the money would long ago have disappeared. So, despite utterances of concern about the low and slow disbursement process, the president cannot be surprised or concerned that the banks are circumspect.

In May already, EOSA had spelt out the devastating impact of lockdown measures on the enterprise world , arguing that the systemic damage caused to the spontaneous order of enterprises can best be ameliorated by a systemic response that would enable the spontaneous order to establish its own patterns again.

The government, however, kept its focus on basically two things:

- Promoting Covid-19 to the highest pedestal of dangers, wilfully ignoring all other existing problems as well as the additional problems the lockdown strategy would create, and

- Pursuing its social engineering efforts to reshape the South African economy in particular, and society at large, by limiting state relief measures to businesses complying with BEE (effectively throttling white sole proprietor businesses to death), deciding which kind of businesses are essential and which not, and pursuing anti-tobacco and prohibition agendas by bans on cigarette and alcohol sales.

The loan guarantee scheme, announced with great fanfare to support businesses as the centrepiece of the R500 billion social and economic recovery package, is still “stuck on the runway”, as economic journalist Ray Mhlaka remarked.

Despite the fact that taxpayers (through guarantees by the Reserve Bank and Treasury) will pick up 94% of the losses on loan defaults, the banks have not disbursed more than a meagre R16 billion (8%). In an attempt to accelerate loan disbursements, the scheme has done away with the turnover ceiling that had limited applicants to enterprises with a turnover under R300 million, effectively enabling all listed companies to also submit loan applications.

The banks who administer the scheme are not flooded by applications: fewer than 50,000 applications have been submitted.

No appetite for bad debt

The main reason for the low number of loan applications is simply that the vast majority of formal businesses in South Africa cannot afford to take on further debt: trading conditions are too problematic given the policy environment, the threat of expropriation without compensation, leg-irons of BEE and a very strict labour dispensation. The fact that the banks who handle the loan applications have granted such a low number of loans also underline their lack of appetite for bad debt. They are not keen to carry that 6% of loan values for debt that cannot be recovered, since that has to come from their reserves. The government, liable for 94% of defaults however, will simply raise taxes, borrow more or embark on strategies of official looting, e.g. expropriation without confiscation and/or prescribed investments.

The CIPC database (which caters only for incorporated businesses, excluding sole proprietors and partnerships) is unreliable and cannot serve as an indicator of the number of businesses. SARS Company Income Tax (CIT) statistics, which also deals with incorporated entities (e.g. companies, close corporations, trusts, cooperatives), had 814,151 taxpayers that had submitted returns for CIT for tax year 2017. The data on the 2018 tax year is still too incomplete to determine the number of actual assessed submissions. Based on the 814,151, less than 6% of formal incorporated businesses had applied for loans with a mere 1.82% successful in obtaining state-guaranteed loans.

A recent report by McKinsey & Company – A Credit Lifeline: How banks can serve SMEs in SA better – comments on the slow disbursements from the loan guarantee scheme, stating that it is especially the middle segment of formal SMEs with a turnover ranging from R1 million to R100 million that struggle to obtain finance.

McKinsey (Figure 1) reckons there are between 160,000 and 540,000 enterprises in this “missing middle” that struggles to obtain loan finance, either for investment or bridging purposes.

In a previous article EOSA has described the loan guarantee scheme for businesses as effective as applying Elastoplast to a cut on a boxer’s cheek whilst he lies unconscious because a knock-out punch.

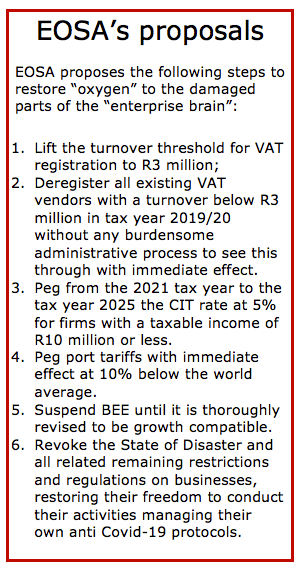

EOSA proposes a number of systemic interventions that will not require lengthy administrative loan applications and evaluation processes, that will systematically give support to all formal businesses in the missing middle (See text box).

These proposals will all have a systemic effect on all enterprises, thus benefitting all and not some. The proposals are quite fundable. EOSA has adjusted the thresholds higher than in the original article because it became clear that the cost of the proposals is miniscule compared to the R200 billion loan guarantee fund, not to mention the other R300 billion component of the ERRP.

These are:

1. Raise VAT threshold to R3 million turnover level

The threshold for VAT registration was last adjusted in 2008 when Trevor Manual raised it from R300 000 to R1 million. If pegged to the inflation rate, it would have risen now to R1.952 million.

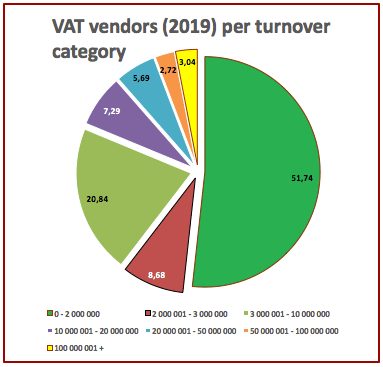

The IMF reckons a low threshold significantly compromises both the political and administrative feasibility of a VAT. Figure 2 reflects the percentage of VAT vendors per turnover category. Of the 449,000 VAT vendors, 51.74% had a turnover below R2 million with a further 8.68% in the turnover bracket R2 – R3 million per annum. By raising the VAT threshold to R3 million at least 225 000 fewer VAT submissions will be required.

Considering the administrative load on and costs for small firms, one would think that the yield of this portion of the VAT vendors would be substantial. However, as illustrated in Figure 3, the firms with turnover below R2 million contributed a mere 1.86% of the total net VAT generated. The VAT vendors with turnover of R2 – R3 million made a contribution of 3.47% of the net VAT yield

Figure 3 shows clearly that these turnover categories have not made a significant contribution over the past 12 years, but it has usurped numerous entrepreneur years that could have been devoted to the strengthening and possible expansion of the formal businesses. Add to this the actual staff and admin costs at SARS, and it is clear that the yield is not worth the effort and cost.

2. Revoke the VAT registration of all enterprises with turnover below R3 million

To ensure this benefit will have immediate effect, in terms of the State of Disaster, the government should deregister all existing VAT vendors with an annual turnover below R3 million. This process should be without a burdensome tedious process and simply place these VAT vendors on an immediate non-VAT footing.

The negative impact on the government’s income will be a mere 5.55% of net VAT income, or R7.8 billion if based on the 2019 VAT data. This pales into insignificance against the billions squandered on the ill-considered pandemic expenditures, not to mention the R200 billion loan guarantee fund. More than 225 000 businesses will be helped by this process.

The cost of business will drop. In especially small firms where business owners devote a disproportionate time to comply with VAT submissions, the heavy burden of regulations will free time to devote to income generating purposes.

It will simultaneously enable SARS to devote its efforts to the big whales that get away, rather than concentrating on the undersized sardines.

3. Cut CIT to 5% for businesses with taxable income below R10 million

South Africa’s CIT rate is 28%, much higher than the 15% of Mauritius, the 17% of Singapore and the 21.5% in the case of Sweden. The impact of lockdown hit the small formal businesses the hardest: their access to finance is more difficult than those of the large businesses, but their commitments (property tax, utilities, loans and salaries) far outstrip the obligations of the informal businesses.

EOSA, therefore, proposes that the CIT rate for all business with a taxable income of R10 million or less should be cut to 5%. Based on SARS’ CIT data for tax year 2017, the 808 000 CIT tax payers with taxable income below R10 million were assessed to be liable for a total of R34.38 billion CIT. By applying a 5% CIT rate for these businesses, an amount of R28.24 billion would stay in the books of the 808 000 companies. This support would enhance the likelihood of business recovery far better than the loan guarantee scheme, since it would benefit 99.23% of all registered businesses.

4. Peg Port duties & tariffs at 10% below the global average

The latest Global Pricing Comparator Study of the Port Regulator of South Africa confirms that:

- Port authority pricing (a combination of cargo dues and marine charges) is 146% above the global sample average, making SA ports the most expensive in the sample studied.

- Terminal handling charges are 117% above the global sample average for 2019.

- Cargo dues for containers in SA ports are 233% higher than the global average.

These administrative costs, handled by the government and its agencies, undermine both the financial and economic positions of South African consumers as well as producers. With the bulk of manufactured and agricultural exports leaving by container, these tariffs are rendering SA producers less competitive and thereby narrowing their margins, mainly to ensure that the National Ports Authority profits can keep the rest of the Transnet group going.

Is it Mr Gordhan again?

Industrial policy aimed at promoting exports is thus undermined by the Minister responsible for State-owned Enterprises in order to keep a struggling Transnet afloat.

Pegging all these charges at 10% below the global average would provide a boost for the total economy at the levels of importers, exporters as well as consumers.

The systemic interventions proposed by EOSA will have an economy wide impact and therefore more effect than a loan guarantee scheme that remains as stuck on the runway as Pravin Gordhan’s SAA Fantasy.